SanDisk: New Price Target Unleashed

We survived a crazy week in the market, and we've got another one coming up!

Now let's jump into what you really want to know:

1. Semiconductor Madness Is On, and JR Has a New SNDK Price Target

This market is all about semiconductors.

The SMH ETF is up over 30% in April, led by monsters like:

Astera Labs (ALAB): +95%

Intel (INTC): +83%

AMD (AMD): +70%

Marvell Technology (MRVL): +65%

On Semiconductor (ON): +59%

And SanDisk (SNDK), which is not in the SMH ETF, is up 56% to finally get past the $1,000 mark.

Our own JR Romero predicted this in February:

Now, JR sees SanDisk going to $1,298.

(we recorded a video this afternoon, but due to an error by yours truly, it was erased)

SMH's RSI is now at 84+, so it looks overheated.

But who wants to step in front of a freight train, especially ahead of a week where multiple tech giants may announce even more increases in capex spending.

The fundamentals support the semis' huge move.

According to FactSet, Semiconductor revenues are expected to grow by a whopping 51% this quarter.

And earnings are expected to grow 98%.

Speaking of earnings…

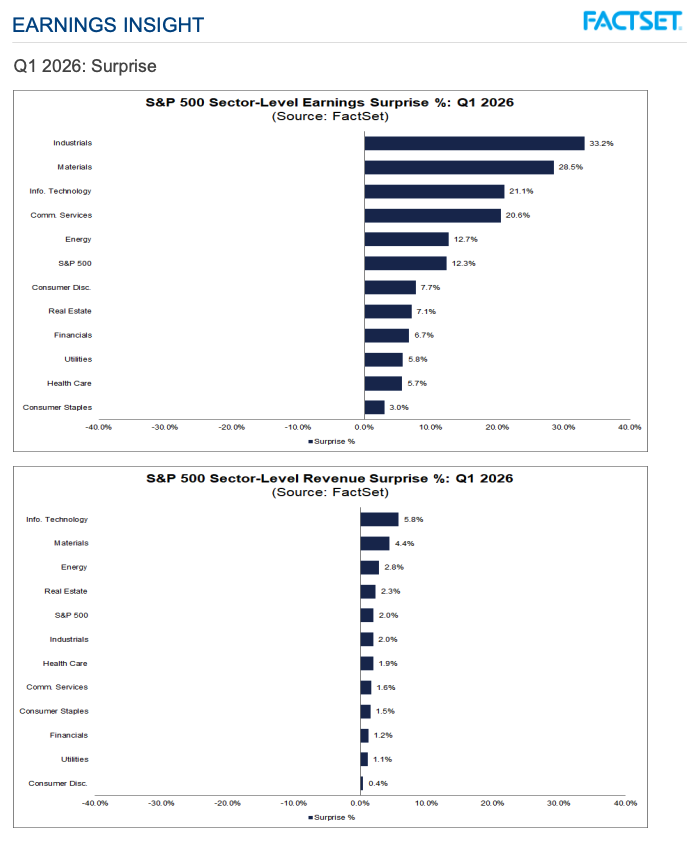

2. Earnings Season Has Been Excellent

According to FactSet, 28% of S&P 500 companies have reported Q1 earnings, and things are looking good.

84% of reporting companies beat earnings forecasts, and 81% beat on revenues. Both are above historical norms.

Analysts expected 13.1% growth at the start of Q1.

Now it's tracking towards 15.1%.

That number could push even higher given all the heavy-hitters yet to report like Alphabet (GOOGL), Apple (AAPL), Amazon (AMZN), and Nvidia (NVDA).

Plus, while tech is a huge driver of the aggregate numbers, every single S&P sector is reporting higher-than-expected earnings and revenues.

For example, we've seen monster results from the likes of GE Vernova (GEV), FedEx (FDX), Newmont (NEM), and Baker Hughes (BHI).

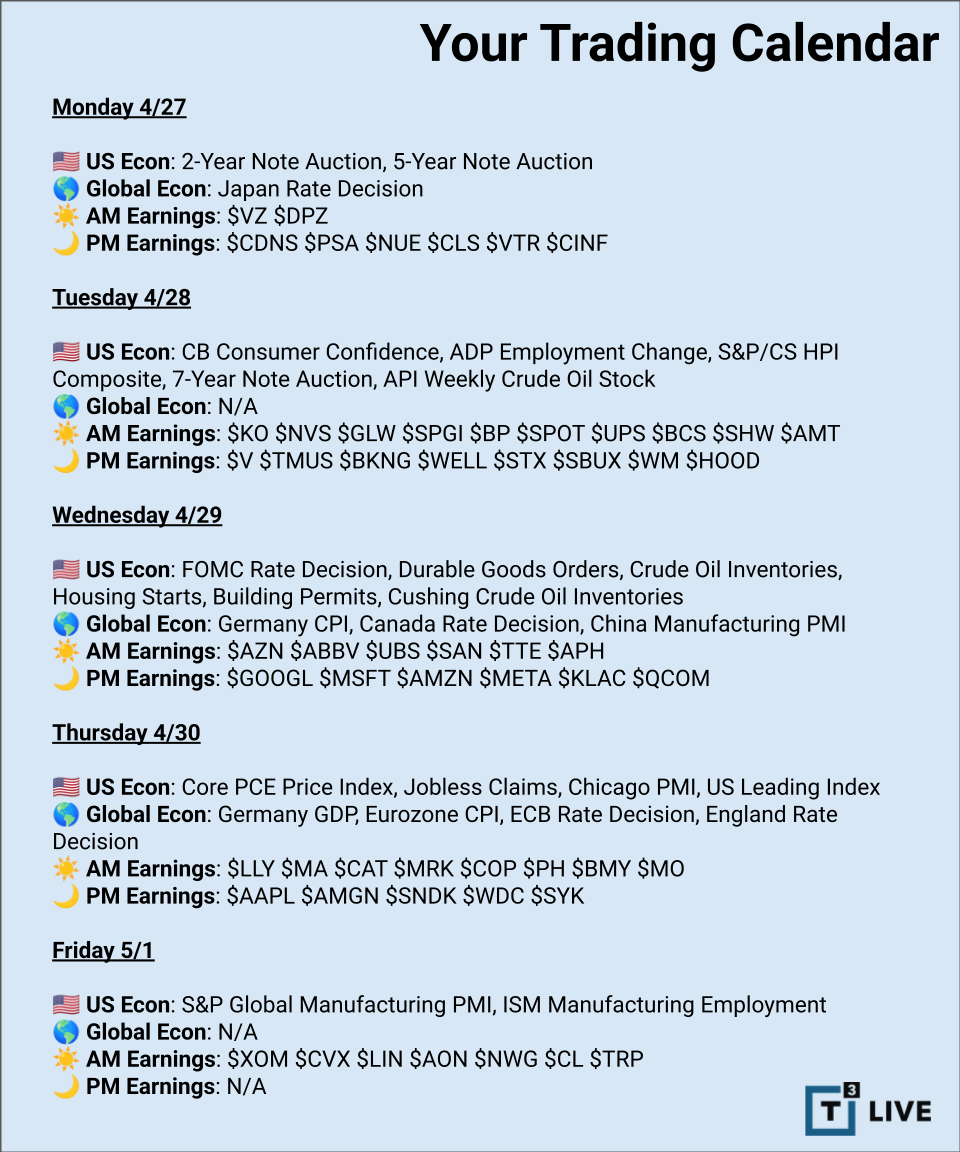

3. It's Time to Buckle Up

If you thought this week was wild, buckle up!

Because we're about to get hit by:

- Rate Decisions from the FOMC, ECB, Bank of Japan, and Bank of England

- Earnings from tech giants Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), Amazon (AMZN), Meta (META), Qualcomm (QCOM), SanDisk, and more

- Additional reports from Visa (V), Starbucks (SBUX), Robinhood (HOOD), Caterpillar (CAT), and Exxon (XOM)

And this doesn't even include what may happen in the Middle East!

Here's the full calendar:

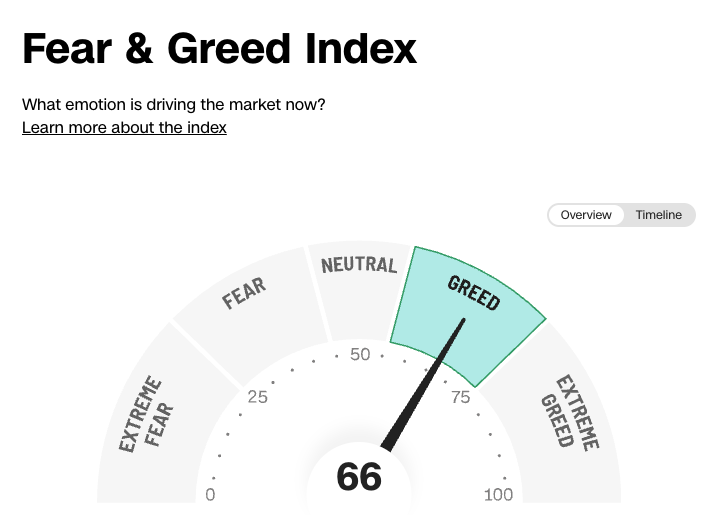

4. Traders Turned Bullish

The latest AAII Sentiment Survey shows that 46.0% of investors are bullish for the next 6 months.

This comes after 9 straight weeks of bearish readings.

Meanwhile, CNN's Fear & Greed Index is at 66 showing modest greed. This is up from just 18 (extreme fear) one month ago.

And as of Thursday's close, the CBOE Equity Put-Call ratio was just 0.51, which means low demand for put options.

This doesn't mean investors and traders are euphoric.

But all-time highs did cheer them up.

5. Avis Was One for the Ages, and Animal Spirits Are Here

This week saw the end of the greatest short squeeze of 2026.

In Avis Budget Group (CAR).

Yes, the car rental company.

The stock went from $100 to $847 in a month.

And then it fell over $600 in two days.

Not because the rental car market went wild.

It's because Deutsche Bank discovered that two investors controlled 108% of shares through derivatives layered on top of normal share ownership.

Momentum buyers piled in, which attracted more momentum.

And more and more and more until there was no one left to buy.

Then everyone hit the exit button at once.

This looked like a more extreme version of Allbirds (BIRD), which had its own wild short squeeze after announcing a transition from sneakers to “AI compute infrastructure.”

I wish I was making that up.

But between Avis, Allbirds, and the semis, one thing's for sure.

The animal spirits are alive.