How This Stock Market Will Top

“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market to-day has happened before and will happen again.” -Edwin Lefèvre, Reminiscences of a Stock Operator.

The term “speculator” has been used derogatorily ever since the 1929 stock market crash. Ben Graham spent an entire chapter in Security Analysis attempting to delineate the differences between investing and speculating. I’ve read that chapter dozens of times over the years in hopes that repetition will bring clarity as to what exactly is the distinction between the two.

All these years later I still can’t believe in a real distinction between speculation and investing, and I don’t think he believed it himself. From what I understand, Ben Graham ran a proto-hedge fund, lost all his investors’ money “investing” according to his method, got a job as a professor teaching others how to do what he couldn’t do for himself, and then spent decades winning back his investors’ lost money. That’s a lot of effort and a lot of years for a scratch trade. If that’s what happened to the genitor of common stock “investing” as we know it today, then for my money, speculation seems like a better approach…

Nowadays it’s almost verboten to refer to your market participation as “speculation.” This wasn’t always the case. It certainly wasn’t the case in the late 1920’s.

I like to surf old New York Times archives from the financial section to get a feel for the zeitgeist from earlier periods in the market. What’s most stunning to a contemporary reader is the brutal honesty with which reporters delivered the financial news. Everyone back then accepted that stock markets were for speculation. There was no need to explain price movement with a fundamental narrative. It was all insiders creating pools and bidding up stocks, or hammering them down.

Today we would call that “insider trading.” While it’s tempting to think so much has changed in the stock market between then and now, I don’t think our markets are very different from markets in the late 1920’s. That’s because human nature never changes.

The quote from Lefèvre stands true: whatever happens in the stock market today has happened before and will happen again.

Deep in the annals of stock market history lie the clues to discern what we are going through in the present. Market quotations, in their essence, are the manifestation of thoughts in the minds of men. To study their recorded thoughts from the past is the closest we can come to gaining their experience, and experience is the most powerful tool we have in attempting to win in the markets.

We can stamp either label we’d like on the activity, whether it’s investing or speculation, but the approach is the same: figure out what has worked in the past, and apply it to the present. This is the way we win in the markets.

As for me, I think it’s all speculation, so we better aim to do it well. Proper investing is merely one element of speculation. You’ve got to have some understanding of basic fundamental conditions to speculate well.

It’s my view that we are in the contraction phase of the business cycle, and that this autumn we will see a window of opportunity for the market to sell. All the conditions are in place: a stock market that requires a lot to go right to justify a 20 PE, a new technology that created a mania and parabolic charts like memory chip stocks, an opaque securitization scheme with leverage in private credit, the largest stocks shifting their capitalization tables from buybacks to debt issuance for AI capex, and now the biggest IPOs in history adding tons of shares on the market. If you were looking for a recipe to make a top in the stock market, you couldn’t ask for better ingredients.

To understand how to speculate in this market properly, I study the past.

The charts of previous market tops show us the subtle clues that revealed the shifting probabilities favoring price declines rather than further increases after a long bull run. Below are two famous crashes we can scour for portents that inside the minds of men, fear was beginning to replace greed, stocks were being distributed from strong hands to weak hands, and the natural proclivity for stock prices was to retreat.

The 1929 and 1987 tops display a certain uniformity in price structure that we can capture and build into a “top template” for memorization and pattern recognition as we move into the window for a crash this autumn of 2026.

While all tops have their own unique characteristics, there are two broad categories of tops I’ve identified from historical studies: autumn tops and spring tops.

1929 and 1987 are autumn tops, and 2000 and 2008 are spring tops.

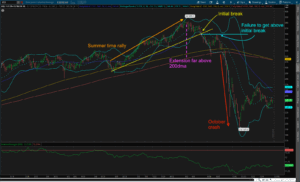

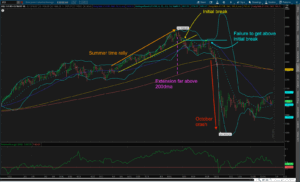

Since we are past the spring window, and the 2026 market most resembles the autumn tops, I’m focusing on those. The autumn tops both share these basic elements in common: a summer time rally, an extension of price far above the 200 day moving average, an initial break, a failure to surpass the initial break price level, and an autumn crash.

Here are annotations of the basic elements on the historical charts of the Dow Jones Industrial Average:.

1929:

1987:

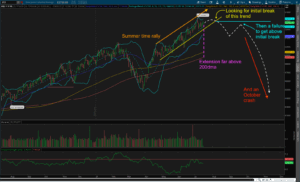

Now here’s an annotation on the current 2026 $DJIA and what I’d expect to happen if this market follows the autumn top template.

2026:

After this summer rally, I’m looking for an initial break sometime in late August or early September, coinciding with back-to-school time when no one besides professional traders will be paying attention to the markets. Everyone will be busy getting back to work and CFO’s will be creating budgets for the next year. This is the earliest an initial break would occur.

The initial break, if it comes, would be our first warning that the market is at risk of following our autumn top template. The market can behave like a wild animal: it doesn’t have to follow our template if it doesn’t want to, so I won’t uphold the initial break as a canon that the market will crash, but I will be on high alert.

I’d then look for acceptance of price below the 50day moving average for some period of time, maybe up to a month or so, as price attempts to retake the previous trend break.

This would be the most crucial time to start paying attention, tightening up stops on tactical trading positions, and trimming strategic long term positions down to a bare minimum. If price on $DJIA is below the 50dma around September, I’d start to prepare for a rejection of price at the initial break level, and short the $SPY and $QQQ on the first red candle at the test of the initial break with a stop right above the initial break level. I’d look to cover around the lows of April, as I think that swift of a decline will bring out policy support from panicked politicians coming back from summer break.

That’s my template for price structure, but price alone is not enough for me to feel comfortable sitting in a large position. I need to have some fundamental backdrop that provides a narrative for a crash. The conditions I’ve mentioned before (parabolic moves in price in the heavily traded theme stocks and a private credit industry that is going to have to mark down assets) are merely the conditions that increase the probability of a crash this autumn.

In order for a crash to occur, we would likely need it to be accompanied by an actual catalyst event that is unrelated to those set up conditions.

In 1929, the catalyst was a surprise 100bps hike by the Bank of England in September 1929 which brought rates higher in London than in New York and made global credit demand more attractive in NY. Farmers would have to go to NY to get credit to undertake the fall harvest, and thus, money had to come out of the financial economy and into the real economy as the USD was still fixed to gold then, so prices crashed.

In 1987, it was the Germans that were hiking rates and US Treasury Secretary Baker was livid that they were going against what they agreed to at the Louvre Accord. Baker wanted Germany to keep a lower interest rate policy and stimulate demand inside their borders. That would draw in imports to West Germany from USA, and reduce the trade deficits of the USA without our Fed needing to raise rates to slow demand for imports or our Treasury to devalue the dollar to stimulate exports. Baker threatened Germany by stating Washington would tolerate further dollar weakness. The market was already leery of the weak USD since the Plaza Accord so Baker’s threat was the catalyst that set off the 1987 crash.

This time, I think the culprit that will set off a crash could be Japan. I don’t know what agreements Bessent has with the Ministry of Finance in Japan, but I’ll bet the Japanese don’t like the Yen above $160. My guess is a surprise rate hike by the BOJ later this autumn to stop the Yen weakness. If that coincides with a break of this current price trend in the $DJIA, I’ll be far more confident in a crash and comfortable holding a short position after a one day failure at the initial break level of the trend in the late September, early October time frame.

I think the quote from Reminiscences is a great heuristic in approaching the market. Another quote I like that is attributed to Mark Twain is also apt: “History doesn’t repeat itself, but it often rhymes.” I don’t think the next stock market crash will repeat exactly like the past ones, but I do think it will rhyme.

_________________________________________

By: Patrick G. Full-time independent trader in Atlanta, GA.

Patrick G is a full-time trader. Worked for a decade in a money management firm as a trader for high net-worth individuals.

He invested his and his family’s net worth into gold and mining stocks before the Covid money printing. Gold and commodity runs of the past 3 years allowed Patrick to trade full-time due to his gains.

Past performance does not guarantee future results. Trading involves significant risk of loss, and individual results vary. Positions mentioned are the author’s own, disclosed for transparency — not individual investment advice.

ATTN: Serious Options Traders

There Is Just ONE Epic Trade Every Week